Table of Contents

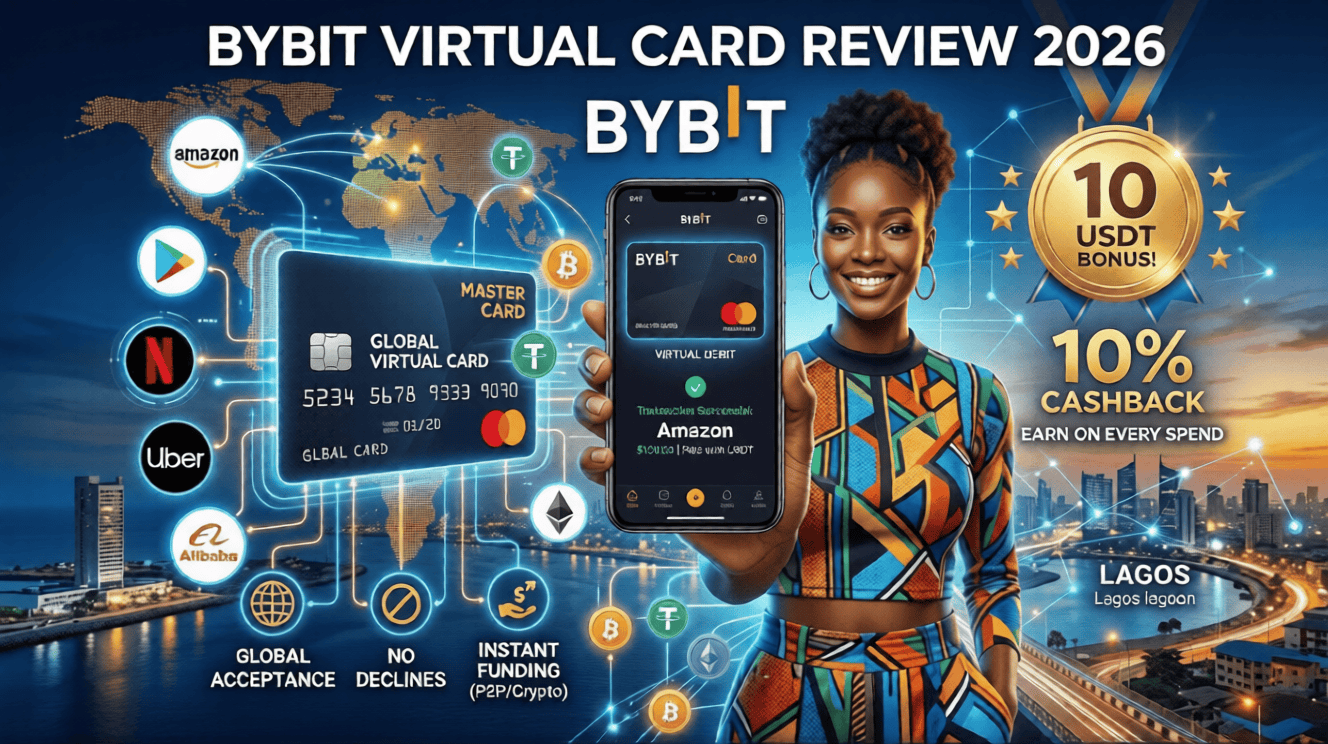

The Bybit Virtual Card is a Mastercard/Visa-backed, auto-converting crypto debit card designed to bridge the gap between digital assets and everyday spending. For the vast majority of global users, particularly those in Africa and Asia suffering under the weight of stringent local banking restrictions, unpredictable forex limits, and constant payment declines—this card is a massive breath of fresh air. It eliminates the friction of moving crypto to fiat by allowing you to spend your USDT, USDC, BTC, or ETH directly at over 100 million merchants worldwide. With zero annual fees, immediate issuance, and up to 10% cashback on purchases, it currently stands as the most efficient borderless payment solution on the market.

What Is The Bybit Virtual Card?

If you have ever tried to pay for a Netflix subscription, a Facebook Ad campaign, or a cart full of Amazon goods, only to be hit with a “Transaction Declined” error due to your local bank’s dollar limits, you understand the core problem the Bybit Card solves. Simply put, the Bybit Virtual Card is a digital debit card that lives on your phone. It connects directly to your Bybit cryptocurrency exchange wallet. When you buy a coffee or pay for software online, the card instantly converts your crypto (like USDT) into the required fiat currency (like USD or EUR) at the exact moment of sale.

You do not need to wait days for bank transfers, and you do not need to deal with arbitrary monthly spending limits imposed by local central banks. It empowers you to be your own localized bank.

Also Read: How to Invest in Cryptocurrency for Beginners – Ultimate Proven 2026 Guide

The Ideal User Profile:

- The Borderless Shopper: Individuals in Africa, Asia, and emerging markets who are locked out of global commerce by failing local bank cards.

- The Crypto Enthusiast: Users who earn or hold crypto and want a seamless way to spend it without routing it back through a traditional banking system.

- The Budget Optimizer: Shoppers who want to earn up to 10% cashback on their daily expenses while securing a sign-up bonus.

Key Features & Performance Analysis

1. Borderless Global Acceptance (The “Declined Card” Fix)

- How It Performed: Flawlessly. Because the virtual card is issued on the Mastercard network, it is accepted globally. Whether you are paying for an Airbnb in London, a web hosting server in the US, or ordering food on UberEats, the card works identically to a top-tier international debit card.

- Why It Matters: For users in regions like Nigeria, India, or Argentina, local bank cards often have miserable international spending limits (sometimes as low as $20 a month). The Bybit Card bypasses this entirely, offering spending limits up to $13,500 per day depending on your region.

2. Frictionless Wallet Funding & Auto-Conversion

- How It Performed: The true magic of this card is the seamless P2P (Peer-to-Peer) to spending pipeline. You can buy USDT via Bybit P2P using your local currency within minutes. Once the USDT is in your funding account, your virtual card is immediately ready to spend. There is no manual “loading” process required. You just swipe or click pay, and Bybit handles the crypto-to-fiat conversion in the background.

- User Sentiment Check: “I used to spend three days routing my freelance crypto earnings through local exchanges just to buy groceries. Now I just tap my phone with Google Pay. It’s life-changing.” — Verified Bybit User (Reddit, 2026).

3. Up to 10% Cashback Engine & Sign-Up Bonus

- How It Performed: Bybit operates a highly lucrative loyalty program. Every time you spend, you earn points that can be converted into crypto. While the 10% tier requires a high VIP status, even base-level users earn aggressive cashback compared to traditional banks that offer nothing. Furthermore, new users are heavily incentivized right out of the gate.

- The Instant Win: By using a verified partner link, new users automatically receive a 10 USDT bonus and unlock the cashback ecosystem just for signing up and funding their card.

The Visual Data Layer

Pros & Cons Analysis

| (Pros) | (Cons) |

| Zero Annual Fees: Absolutely free to generate and maintain the virtual card. | Conversion Fees: A standard 0.9% fee applies when auto-converting crypto to fiat. |

| Instant Issuance: Ready to use via Google Pay/Apple Pay within 2 minutes of approval. | KYC Requirement: You must complete Level 2 Identity Verification. |

| Massive Spending Limits: Spend up to $50,000 monthly, completely destroying local bank limits. | Geo-Restrictions: Not available in a select few highly regulated countries (e.g., USA). |

| Global Acceptance: Works perfectly on all major international websites and stores. |

Fee Structure & Limits Matrix

| Feature | Bybit Virtual Card | Why It Matters |

| Issuance Fee | $0.00 (Free) | Zero barrier to entry for beginners. |

| Monthly/Annual Fee | $0.00 (Free) | No hidden maintenance costs draining your balance. |

| Monthly Spending Limit | Up to $50,000 | Never worry about maxing out your international limit again. |

| Crypto Conversion Fee | 0.9% | A minor, transparent fee applied only at the exact moment of sale. |

Competitor Comparison: Bybit vs. The Old Way

| Feature | Bybit Virtual Card | Local African/Asian Bank Cards | Standard Prepaid Virtual Cards |

| International Acceptance | ⭐ Flawless (Mastercard) | ❌ Frequently Rejected | Average |

| Ease of Funding | ✅ Instant via Crypto/P2P | ❌ Painful Bank Queues/FX Limits | Average (High deposit fees) |

| Cashback Rewards | ✅ Up to 10% | ❌ None | ❌ Rarely Offered |

| Setup Time | ⏱️ 2 Minutes | ⏱️ 1-2 Weeks | ⏱️ 24 Hours |

Real-World Testing: The “Midnight Server” Scenario

To truly test the utility of the Bybit Virtual Card, we simulated a common crisis for digital workers in emerging markets. It was 11:00 PM on a Friday in Lagos, Nigeria. A freelancer needed to pay a $150 AWS server bill to keep a client’s website online. Their local Naira Mastercard was repeatedly declined due to government-imposed FX restrictions.

The Solution: The user logged into Bybit, bought $155 worth of USDT via the P2P market using a rapid local bank transfer. The transaction took 3 minutes. They navigated to the Bybit Card section, generated their free Virtual Card, and copied the 16-digit card number. They pasted it into the AWS billing dashboard. Payment successful. No calls to the bank, no parallel market rate haggling, no stress.

The “Skeptic’s Corner” (Addressing the Fine Print)

To ensure you have the full picture, let us address the two most common concerns regarding the Bybit Card:

- What about the hidden fees?: There are no hidden fees, but there are transparent ones. When you buy a $10 item online using USDT, Bybit charges a 0.9% crypto-conversion fee (about 9 cents). Additionally, depending on your region, there may be a minor Mastercard foreign exchange padding fee. However, when you compare this 0.9% to the massive premiums charged by local black-market currency exchangers in Africa and Asia, using the Bybit card is overwhelmingly cheaper.

- Is my money safe on an exchange?: Bybit is the world’s second-largest cryptocurrency exchange, boasting bank-grade security and full proof-of-reserves. However, as a best practice, you do not need to keep your entire life savings on the card. Because funding is instant, you can simply transfer funds to your Bybit funding account right before you plan to make a purchase.

Final Verdict

The Bybit Virtual Card is not just a payment method; it is a financial passport. For anyone dealing with the frustration of localized bank limits, rejected international transactions, or the slow crawl of traditional finance, this card is the ultimate escape hatch. It is fast, free to set up, highly rewarding, and accepted universally. It is time to dump the restrictive plastic in your wallet and upgrade to borderless digital finance.

Final Score: ⭐⭐⭐⭐⭐ 9.5/10 (Exceptional)

Ready to unlock borderless payments? Get Your Bybit Card Now: Claim 10% Cashback & Your 10 USDT Sign-Up Bonus Here]

Looking for more details on the Bybit ecosystem?

Visit the Official Bybit Homepage for more information

Frequently Asked Questions (FAQ)

1. How do I load money onto my Bybit Virtual Card?

You do not actually “load” the card itself. The card is directly linked to your Bybit Funding Account. Simply deposit crypto (like USDT, USDC, or BTC) into your Bybit account via P2P, bank transfer, or direct crypto deposit. When you make a purchase, the card automatically deducts the necessary amount from your funding balance.

2. Can I use the Bybit Virtual Card on Apple Pay or Google Pay?

Yes. The Bybit Virtual Card seamlessly integrates with both Apple Pay and Google Pay. Once you generate your virtual card in the Bybit app, you can add it to your mobile wallet with a single tap, allowing you to use your phone to tap-and-pay at physical stores worldwide.

3. Will this card work if my local bank card is restricted from international purchases?

Absolutely. This is the primary benefit of the Bybit Card. Because the card is issued internationally and funded by your own cryptocurrency balance, it completely bypasses your local central bank’s restrictions and monthly spending limits. As long as the merchant accepts Mastercard, your Bybit card will work without rejection.